Introduction

Healthcare practices run on thin margins with enormous fixed costs — and payers rarely make that easier. Insurance companies, Medicare, and Medicaid routinely take weeks to months to process and pay claims, while payroll, supplies, and facility overhead come due on schedule regardless of what's sitting in accounts receivable.

According to Crowe's 2023 healthcare revenue cycle scorecard, the average true days in A/R for healthcare organizations sat at 55 days, with commercial payer receivables over 90 days reaching 34%. For smaller practices and specialty clinics, that gap between service delivery and payment can create a real liquidity crisis.

Medical receivables factoring is one financing tool designed to close that gap — converting outstanding insurance claims into immediate working capital. This guide covers how the process works, what drives costs and eligibility in a healthcare context, and when factoring makes sense versus when a different financing structure fits better. It's written for small-to-mid-sized practices, specialty clinics, staffing agencies, and medical suppliers dealing with slow payer reimbursements.

Key Takeaways

- Medical receivables factoring converts unpaid invoices into immediate cash — structured as a sale, not a loan, so it creates no debt

- Factors typically advance 75–95% of invoice value upfront, collecting the balance minus a discount fee once the payer remits

- Approval depends on the payer's creditworthiness (insurer, Medicare), not the provider's — making it accessible to newer or credit-thin practices

- Healthcare factoring adds complexity: HIPAA compliance, government payer restrictions, and payer mix all affect eligibility and terms

- Factoring works best as bridge financing — not a replacement for strong billing practices or lower-cost credit options

What Is Medical Receivables Factoring?

Medical receivables factoring (also called medical invoice factoring or medical accounts receivable factoring) is a financing arrangement in which a healthcare provider sells its outstanding invoices to a third-party factoring company at a discount in exchange for immediate cash. Those invoices represent amounts owed by insurers, Medicare/Medicaid, or patients for services already delivered.

The goal is straightforward: convert accounts receivable into working capital now, rather than waiting 30 to 120 days for payer reimbursement. That cash covers payroll, medical supplies, rent, and the other operating expenses that don't pause while insurers process claims.

How It Differs from Related Financing Structures

Two distinctions separate factoring from similar-sounding arrangements:

Factoring vs. a business loan:

- A loan involves borrowing money and repaying it with interest

- Factoring involves selling an asset (the invoice) — no debt is created, no interest accrues

- This distinction matters for balance sheet treatment and debt covenant compliance

Whether a factoring arrangement qualifies as a true sale depends on whether it meets the criteria under FASB ASC 860. Transactions that don't fully satisfy those criteria may still be recorded as secured borrowings on the balance sheet.

Factoring vs. accounts receivable financing:

- In AR financing, receivables serve as collateral for a loan; the provider retains collection responsibility

- In factoring, the factor purchases the invoices outright and assumes collection responsibility

Why Medical Receivables Factoring Is Used in Healthcare

The Structural Payment Delay Problem

Healthcare billing operates on a multi-payer system with widely varying reimbursement timelines. Medicare electronic clean claims carry a 14-day payment floor, with interest triggered if payment doesn't occur within 30 days. Medicaid requires 90% of clean claims to be paid within 30 days and 99% within 90 days under federal regulations.

Commercial payers are much slower. Crowe's 2023 analysis found that 31% of commercial inpatient claims remained unpaid beyond 90 days, compared to 12% for Medicare. Commercial payers also initially denied 15.1% of claims in Q1 2023, versus 3.9% for traditional Medicare.

For a practice that bills primarily commercial insurance, the combination of slow payment and high initial denial rates can leave a significant share of earned revenue in limbo for months.

The High-Cost Operating Environment

Delayed payments wouldn't be as damaging if operating costs were deferrable. They aren't. Clinical payroll, malpractice premiums, medical supplies, and facility overhead continue on fixed schedules. According to MGMA's 2025 data, 90% of medical groups reported higher year-over-year operating costs, with an average increase of approximately 11.1%. Support staff salaries and benefits alone typically account for 25% of total practice revenue.

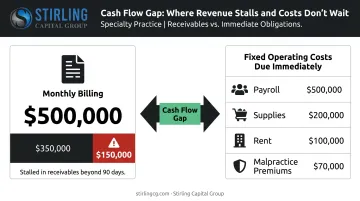

Consider a mid-sized specialty practice billing $500,000 per month: if 30% of its commercial receivables stall past 90 days, that's $150,000 in earned revenue that hasn't converted to cash — while payroll and supplies still need to be funded this week.

Why Approval Is Payer-Based, Not Provider-Based

Factoring qualification is built around the creditworthiness of the payer — the insurer or government program responsible for the invoice — not the healthcare provider's own credit profile or business history. This means:

- Newer practices without established credit histories can qualify

- Practices with thin margins or inconsistent revenue cycles remain eligible

- Providers declined for traditional bank financing frequently qualify through factoring instead

Strong receivables and weak balance-sheet metrics often coexist in healthcare — factoring is structured for exactly that profile.

Who Uses Healthcare Factoring

Two distinct categories of healthcare businesses use factoring:

- Direct care providers — physician practices, dental offices, behavioral health clinics — who factor invoices billed to insurers and government payers

- Healthcare vendors — staffing agencies, medical supply companies, billing service firms — who factor invoices billed to medical practices rather than payers directly

SFNet has documented factoring facilities for healthcare staffing agencies ranging from $1 million to $3 million, structured against commercial insurance receivables — confirming both categories as established use cases.

Regulatory Complexity in Healthcare Factoring

Healthcare factoring is more complex than standard invoice factoring for three reasons:

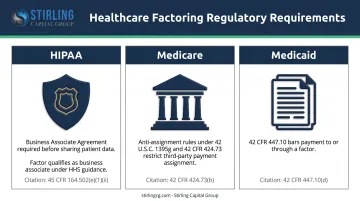

- HIPAA: Any factoring company that receives patient health information during invoice processing qualifies as a business associate under HHS guidance. A signed Business Associate Agreement (BAA) is required before any patient data is shared.

- Medicare anti-assignment rules: Federal law (42 U.S.C. 1395g and 42 CFR 424.73) generally prohibits assigning Medicare payments to third parties, including factoring arrangements — a restriction CMS applies to financing transactions.

- Medicaid prohibitions: 42 CFR 447.10 specifically bars Medicaid payment to or through a factor, defined as any entity that advances money against receivables and charges a fee.

Each of these rules requires factoring structures that are purpose-built for healthcare — general-purpose factoring agreements rarely account for them.

How Medical Receivables Factoring Works

The end-to-end process follows a consistent sequence:

Provider renders service → generates and submits invoice to payer → submits invoice to factor → receives upfront cash advance → factor assumes collection responsibility → payer remits to factor → factor releases reserve balance minus discount fee to provider

Step 1: Invoice Submission and Agreement Setup

The provider selects a factoring company and submits invoices for review. The factor evaluates payer creditworthiness, verifies invoice accuracy, and establishes agreement terms including:

- Advance rate (typically 75–95% of invoice face value)

- Discount fee structure (rate and any time-based scaling)

- Credit line maximum

- Notification policy (whether the payer is informed the invoice was sold to a third party)

Some factors require a Deposit Account Control Agreement (DACA), which gives them control over the bank account where payer payments are deposited.

For government healthcare receivables, this structure needs additional care. CMS rules mandate that Medicare and Medicaid payments be directed to accounts in the provider's own name, which constrains how deposit-account control can be structured.

Step 2: Advance Payment to the Provider

With the agreement finalized, the factor issues an advance (the agreed percentage of invoice face value) via wire transfer. The remaining balance is held in a reserve account pending payer collection.

Advance rates vary based on:

- Payer type (Medicare receivables typically support higher advance rates than self-pay)

- Invoice volume and consistency

- The factor's assessment of collection risk

Step 3: Collection and Final Settlement

The factor contacts payers to redirect payments and manages the collection process. Once the payer remits, the factor:

- Deducts its discount fee from the collected amount

- Releases the reserve balance to the provider

If a payer partially denies or underpays a claim, the final settlement adjusts accordingly. Two structural options govern what happens if a payer doesn't pay at all:

| Recourse Factoring | Non-Recourse Factoring | |

|---|---|---|

| Default risk | Provider repays the advance | Factor absorbs the loss |

| Cost | Lower fee | Higher fee |

| Coverage | N/A | Payer insolvency only — not claim denials from billing errors |

| Availability | More common | Less common |

Key Factors That Affect Medical Receivables Factoring

Payer Mix

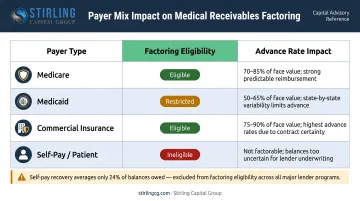

Payer composition drives factoring eligibility and terms more than any other single variable. According to CMS National Health Expenditure data for 2024, private insurance accounts for 31% of total U.S. health expenditures, Medicare 21%, and Medicaid 18%. For hospitals specifically, KFF data shows Medicare accounting for 25% and private insurance 37% of spending.

How payer mix affects factoring:

| Payer Type | Factoring Eligibility | Typical Advance Rate Impact |

|---|---|---|

| Medicare | Generally factorable with compliance steps | Favorable — reliable but requires CMS-savvy factor |

| Medicaid | Restricted; anti-factor rules apply | Requires specialized approach |

| Commercial insurance | Factorable; varies by carrier | Moderate — denial rates affect risk assessment |

| Self-pay / patient balances | Typically ineligible or very low advance | Unfavorable — providers collect only ~24% of self-pay balances owed after insurance |

Practices with heavy self-pay or Medicaid concentration will find fewer eligible receivables and less favorable terms.

Fee Variability and True Cost Calculation

Factoring fees are not fixed annual rates. They compound based on how long a claim takes to collect — a 2% monthly fee on a claim paid in 30 days is very different from the same fee on a claim paid in 90 days.

Direct comparisons to traditional loan rates are difficult as a result. A better approach: calculate total cost per invoice cycle using these three steps:

- Take the discount fee charged by the factor

- Divide it by the advance received

- Annualize based on your practice's actual average collection time

This gives a comparable effective cost for evaluating whether factoring is more or less expensive than a revolving line of credit for a given payer mix.

Notification Policy and Payer Relationships

Beyond cost, how a factoring arrangement is structured operationally can affect payer relationships — making notification policy a key term to negotiate.

- Notification factoring: The payer is informed the invoice was sold. Required by many payer contracts and regulatory rules in healthcare.

- Non-notification factoring: The payer relationship appears unchanged from the provider's side.

In healthcare, notification is frequently required by payer contract terms or regulatory requirements. Providers should confirm whether their agreements permit assignment of claims before signing, and understand how notification affects ongoing payer relationships.

Common Misconceptions and When Factoring May Not Be Appropriate

Two Misconceptions Worth Clearing Up

"Factoring is only for financially distressed practices." Not accurate. Financially healthy practices use factoring proactively to smooth cash flow, fund growth, or bridge seasonal volume gaps — without waiting out slow payer cycles.

"Factoring is a type of loan." It isn't. Factoring is the sale of an asset. This distinction affects balance sheet treatment (factored receivables are removed from the asset ledger if the transfer qualifies as a sale under ASC 860) and may affect debt covenant compliance for practices with existing credit facilities.

When Factoring Is Not the Right Solution

Factoring does not fix operational problems — it only accelerates collections on invoices that are already eligible and accurate. Avoid relying on factoring when:

- High claim denial rates or billing errors are the root cause of cash flow problems. Factoring ineligible or error-prone invoices won't generate the expected advance, and fixing billing processes would address the problem more directly.

- The patient base is predominantly self-pay. Most self-pay receivables won't qualify, and those that do will attract low advance rates.

- Lower-cost options are available. Established practices with strong credit histories and consistent revenue often qualify for revolving lines of credit or working capital loans at lower effective rates.

Warning Signs Factoring Is Being Used by Default

- Factoring all invoices regardless of actual cash flow need

- Factoring fees consistently consuming a material share of net collections

- Using factoring as a workaround for unresolved billing inefficiencies

If any of these patterns are present, the cost of factoring is likely outweighing its convenience, and a more permanent financing structure warrants a closer look. Stirling Capital Group works with over 60 private lending sources and can help practices determine whether factoring, an ABL revolving facility, or another structure better fits their payer mix and cash flow cycle.

Conclusion

Medical receivables factoring converts accounts receivable into immediate working capital without creating debt — making it a practical option for healthcare providers who serve creditworthy payers but face structural payment delays. Its value depends on applying it correctly: matching it to an eligible payer mix, understanding the true total fee cost across the collection cycle, and treating it as bridge financing rather than a substitute for sound billing operations.

That bridge financing decision is worth comparing against other options. Revolving credit facilities, working capital loans, and asset-based lending arrangements may offer lower effective costs for practices with the right profile — and the right structure depends entirely on the practice's payer mix, cash flow timing, and growth stage.

Stirling Capital Group provides access to over 60 private lending sources, including specialty finance providers experienced in healthcare receivables. The focus is on matching each practice's situation to the right lender structure — not defaulting to the most available one. Reach out for a free consultation to evaluate your options with no obligation.

Frequently Asked Questions

What is the accounts receivable process in medical billing?

The core steps are charge capture, claim submission to the payer, payment posting, denial management, and patient billing for any remaining balance. Claim denials and slow payer processing are the most common sources of delay — each one extends the gap between service delivery and payment.

Can you factor Medicare receivables?

Yes, but the arrangement must comply with CMS assignment rules under 42 U.S.C. 1395g and 42 CFR 424.73, including deposit account requirements specific to government payers. Work with a factoring company that has direct healthcare billing experience to structure this correctly.

What are the key Cs of medical accounts receivable management?

The framework covers Capture, Clean, Collect, and Control — disciplines designed to reduce days in AR, cut claim denials, and keep revenue cycle performance tight. These should be functioning well before adding factoring, since external financing can't fix problems rooted in poor claims submission.

What is the difference between medical factoring and a traditional business loan?

Factoring involves selling invoices — an existing asset — and creates no debt or repayment obligation. Approval depends on the payer's creditworthiness. A business loan involves borrowing funds that must be repaid with interest, and approval depends heavily on the borrower's own credit profile, financial history, and ability to service debt.

What are typical advance rates and fees for medical receivables factoring?

Advance rates typically range from 75–95% of invoice face value, depending on payer type, invoice volume, and collection risk. Discount fees vary by factor, payer mix, and how long claims take to collect — making total cost a function of collection speed as much as the stated fee rate. Always calculate cost per invoice cycle, not just the headline percentage.

Is medical receivables factoring suitable for practices with bad credit?

Yes. Approval is based primarily on the payer's creditworthiness, not the provider's — making factoring accessible to newer practices, those with limited credit history, and those declined for traditional bank financing. The strength of your receivables matters far more than your balance sheet.